{kind=link}

The market continues to navigate a complex mix of seasonal demand patterns, weather volatility, and fluctuating supply and demand. To better understand where the natural gas market might be heading this summer, let’s take a look at the latest trends in prices, storage, and weather forecasts.

Current Prices Vs. Price Spread 10 Days Before Expiry Since 2010

The 2025 summer contracts are trading still above the median expiration price, but remain within the interquartile range. Winter 2026 contracts declined relative to the previous week but remain higher than 2025, similar dynamics can be seen in 2027. The market is slowly but still starting to stabilize.

*The graphs were constructed and based on an analysis of data from Bloomberg and EIA.

Forward Curve vs. 2020-2024

A strong upward skew on the curve persists through 2025 despite last week’s price decline. The shape of the curve after 2027 is still more stable, and the decline in outright contract prices has not changed it. It is still in a price range close to the corresponding 2023-2024 curves for the same period of the year.

Current Inventory and Forecast for Next Week Compared to 2019-2024

For week 26 (June 21-27) we expect a 45 BCF increase in storage. The filling level will be above the median for the previous 5 years. In spite of falling pumping rates, if the current supply and demand situation persists, the peak level of 2024 is possible. The weather in the second half of summer remains a constraint.

Weekly HDD+CDD Total from Current NOAA Data and Forecast for the Next 2 Weeks, Comparing 1994-2024

Explanation of the chart: in candlesticks quantiles for 30 years from 1994 to 2024. Red dots 2024, green 2025, blue prediction 2025

Conclusions: HDD+CDD values in the first half of June were below the median. Week 27 (June 30-July06) is expected to be still hot relative to the last 30 years. Forecast values for week 28 are on the upper quantile.

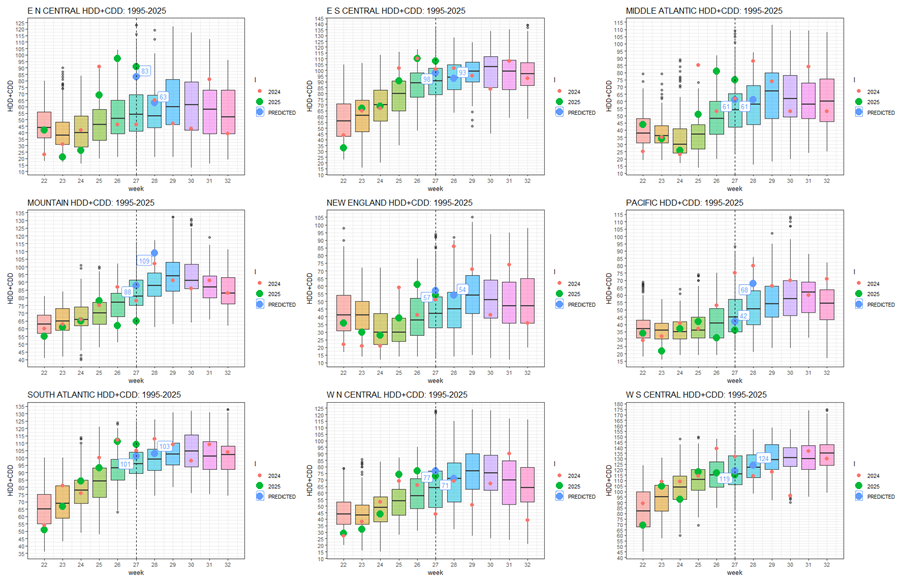

Weekly HDD+CDD total from current NOAA data and forecast for the next two weeks compared to 1994-2024 by regions

If we take a look at regions, we see forecast values for the current and next week above average in almost all regions.

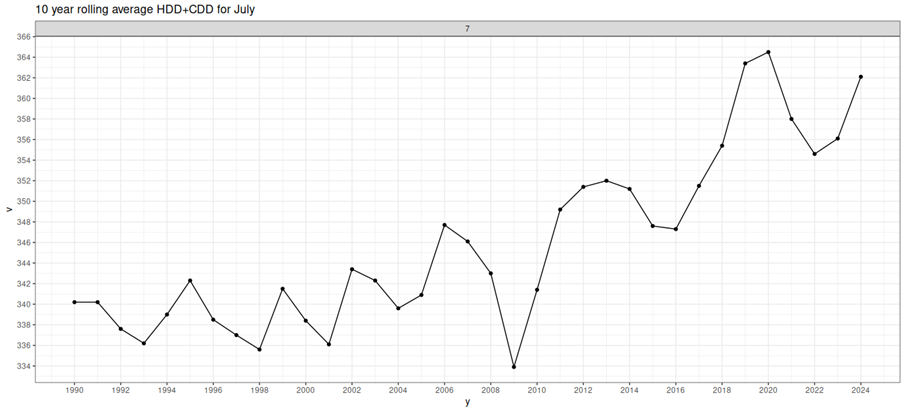

Change in Monthly Weather Averages for 10 years from 1990 to 2024

July has gotten 20 HDD+CDD units hotter over the past 30 years

Weekly Cumulative Supply/Demand Difference Compared to 2014-2024

The April-June 2025 supply/demand balance data is well below the 10-year median due to low temperatures in the first half of summer. The last two weeks have seen a trend reversal towards a higher balance above the historical median. At the same time, due to production growth over the last week, we are watching whether the increased demand from consumption will be compensated by production growth or not.

Percentage change in Spot and nearby futures price relative to the beginning of the year for 2010-2025 by month

Based on 15 years of statistics, spot and near-term futures are trading with minimal divergence in July.